| © 2022 Black Swan Telecom Journal | • | protecting and growing a robust communications business | • a service of | |

| |

| Email a colleague |

December 2021

GCX Builds a Layer 1 Subsea OSS: Wavelengths to Data Centers & Persistent Edge Connectivity for Clouds

Subsea cables are among the roughest and hardest-working digital systems you’ll find anywhere.

And talk about a harsh environment: subsea cables work on the ocean’s floor, about 4,000 meters deep on average in the Pacific. That depth is six (6) times lower than the so-called “crush depth”, the depth at which a modern naval submarine’s hull will collapse from severe water pressure (about 69 times atmospheric pressure).

Twenty-four hours a day, seven days a week sea cables relentlessly toil — in a place where the sun never shines — as they transport 95% of world’s international data traffic. And as best they can, subsea cables live in harmony with some pretty fierce-looking neighbors: the ViperFish, CookieCutter Shark, and the Whiplash Squid, to name a few.

Now as long as a subsea cable is fed a steady flow of electric power, it doesn’t complain. But whenever its lights go dark and the data-packet-conveyor stops, its distress cries grow pretty loud. And then the cable owner — feeling the sudden weight of huge sunk investments earning zero revenue — reliably comes to the rescue.

Sometimes landslides, earthquakes, and ships dragging anchors can injure or even burst a sea cable’s data artery. But fortunately, in a few short weeks, a repair ship will sail to stitch in new tubes, dress up wounds, and bring it back to full health.

When the massive Tohoku Tsunami hit eastern Japan in 2011, dozens of cables on that coast were taken down. Even still, after a tiresome, months-long repair effort, every one of the damaged cables was brought back on-line.

Now beyond natural disasters, another cause of subsea cable stress is the threat of financial miscalculation. You see, the subsea business is competitive and the cost of building and deploying subsea cables runs into hundreds of millions of dollars. So it’s no surprise that owners can overextend themselves and then have to divert their capex to other priorities.

But not to worry: subsea cables are happy to work for a new boss. When it’s time for a cable owner to sell, the investors who are banking the cable find a new operator to get the business moving again.

Regardless of the domain’s inevitable ups and downs, the subsea telecom business is actually a solid and resilient one for two good reasons: 1) Global internet and cloud capacity is expanding, which means subsea cables hold enormous and enduring commercial value; and 2) The business is in the good hands of a travelling band of domain experts — technical and executive veterans who have worked and nurtured the subsea and data center business for decades.

Joining us now is one of those veterans, Jim Fagan, Chief Strategy and Revenue Officer of Global Cloud Xchange (GCX), a leading global provider of subsea connectivity, specifically in the Asia Pacific region, and operator of the world’s largest subsea cable system.

Jim gives us a wonderful tutorial on the business of subsea cables. He begins by explaining the basics of growing subsea capacity and gaining fresh landings. He then explains why GCX is building a Layer 1 OSS to manage its worldwide subsea infrastructure — and the benefits that subsea SDN will bring to data center and cloud customers. And along the way, Jim sheds some important light on how edge computing, clouds, and subsea cable will work together to deliver advanced IoT use cases such as the connected car.

| Dan Baker, Editor, Black Swan Telecom Journal: Jim, it would be great if you could begin by giving us a bit of the history behind GCX, your subsea cable business, and the recent new ownership of the company. |

Jim Fagan, Chief Strategy & Revenue Officer: Sure, Dan. GCX was formerly the international connectivity and subsea business of Reliance Communications (R/COM).

Over the last few years, the parent company, R/COM and GCX ran into financial trouble. So GCX then declared bankruptcy at the end of 2019. Then GCX was formally separated from R/COM and today is a completely independent firm.

New management was brought in May/June 2020. Subsequently, the new team reversed the company’s bankruptcy position in 2021. In November 2021, we announced that GCX was acquired by 3i Infrastructure Group, a leading international Private Equity firm. The investment yielded around $512 Million, resulting in 3i’s 100% ownership position in GCX.

GCX’s key asset is our subsea cables. For instance, our FA1 (Flag Atlantic) offers a north/south route from New York to London and into Paris. Then there’s the HAWK cable that goes from Marseilles down to the Suez.

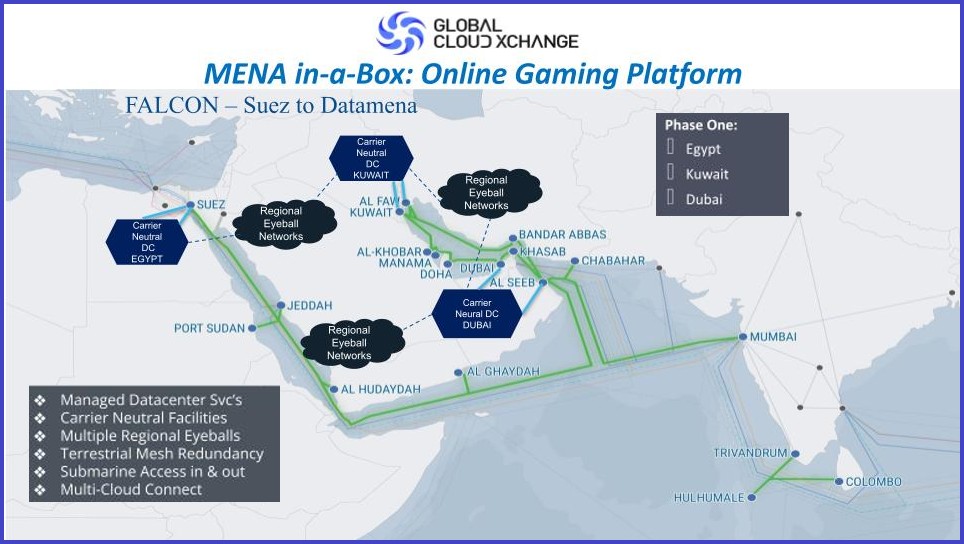

One of our most valuable cables is FALCON which runs from the Suez, does a full loop in the Gulf — landing at every country in the Persian Gulf (which is unique) — then travels from there to India.

In Asia, we have the FNAL system (Flag North Asia Loop). And that’s a jointly owned cable between ourselves, PCCW Global, and Telstra. That cable does a full loop from Korea, Japan, Taiwan, and into Hong Kong, and then from Hong Kong back up to Japan and Korea creating a diverse route. It was a 12 fiber pair system, and GCX owns 4 or 5 of the pairs. Now an interesting point is the partners manage the landing stations jointly, which means sometimes we compete and sometimes we partner.

| What’s your strategy in Asia Pac? And how do you go about balancing your current capacity and planning to bring new cables on-line? |

It’s really about having connectivity and capacity in the key markets we are pursuing. We want to reach growing markets and ones where it’s complex to do business.

This is why serving Asia Pacific is a heavy focus and of great importance to GCX. In Asia, we want to get customers into countries where we don’t land today. So a key strategy of ours is to acquire significant capacity to interconnect Taiwan, Singapore, and India.

If you look at our footprint, we are definitely a go-to for U.S. OTT companies. That includes both Facebook (Meta) and Google as well as the gaming companies, SaaS platforms and more.

Today, by the way, we have plenty of room to light up a new cable: I still have about 70% headroom to sell bandwidth on existing cables — and that’s using current technology. Plus I know many new cables are coming and each of them will take 3 to 4 years to get deployed.

A rule of thumb says the technical life of a cable is 25 years, but we’ve done better than that. Even for our two oldest cables FA-1 and FNAL, we don’t see any technical issues going into the 2030s, which would put them beyond 30 years life.

Now the economic life of a cable varies a bit because subsea is expensive to upkeep. So at some point it might be too high a cost to maintain. But, once again, that’s not a near-term concern.

Actually, it’s funny, Dan: in terrestrial systems, no one ever asks: how old is your fiber? But when people think about subsea, everybody worries about age and capacity.

Yet I’ve got a background in data centers, so I can tell you: the business of data centers is building NEW data centers. It’s just a question of when, where, and how the market is progressing. Meanwhile, those old data centers stay up and keep kicking off cash.

| O.K, let’s talk about your new in-house development effort to build an OSS on top of your subsea cables. What’s the purpose of this move? |

Dan, it’s basically about turning our subsea cables into a software platform. We’re already good at getting the capacity into a country thanks to our relationships and landing sites. Now we aim to unlock our network at Layer 1 so we can start building more intelligent services — and even allow customers to flex their capacity.

We actually have more than a decade of experience building advanced subsea OSS systems. It started with my team at PacNet which later moved to Telstra. Our CTO Jon Vestal was the guy who built all our management capability at GCX.

Before joining GCX, we were the first ones to virtualize layer 2 and spin up services on demand. We used our own routing protocols — not the IP protocol — but our own internal routing tables to pick the best path or worst path — and charge for that.

Of course, back then you could never really create an OSS in layer 1 because the DWM and SLT transponders didn’t have that intelligence. But now that the SDN trend has caught fire, all the subsea cable makers — the Ciena’s and Cisco’s of the world — are opening up their platforms.

Ciena, for instance, has an MCP (Management Control Plane) platform, basically a suite of APIs and services that allow you to start lighting things up and turning things down in Layer 1.

Now if you have only one subsea cable and you’re using your vendor’s MCP, that’s a good way to go. But GCX is in a different situation: we go to many, many markets and our ecosystem is quite a bit more diverse.

Actually, Blue Planet, a Ciena company, has positioned itself as a tool provider to integrate multi-vendor MCPs. Trouble is, their solution is not interoperable enough with their underlying vendors, and that’s a big issue when I’m hooking into a telecom in Korea yet the layer 1 management platforms are not in sync.

So this is what our G360 initiative is all about. G360 is the custom Multi-Domain Controller we are building to orchestrate at the Layer 1 level between all the different devices we use. And once Layer 1 is opened up and virtualized, we can offer unmatched connectivity and flexibility to local data center providers and global network operators.

| Are you saying, for example, you could dedicate a single color wavelength on the subsea cable to a particular data center in Jakarta? |

Exactly. And also allow that data center in Jakarta to change their connectivity: move that wavelength to another data center next month if they choose to.

A customer will come into a GCX portal and see our entire subsea network and where we interconnect. The platform will unlock all sorts of flexibility for them, so this is why we’re excited about G360.

We can start doing interconnecting networks and doing bilateral partnerships where the partners’ terrestrials are moving seamlessly. So this will really unlock the value of our core subsea network, which is one of the biggest in the world.

And we also reach some of the hottest, yet difficult-to-reach markets in the world. So that’s the evolution.

| Looking to the future, how do you see advanced IoT and 5G evolving? How will the cloud, edge devices, data centers, and subsea cables work together in use-cases such as connected cars? |

Actually, Dan, I was amazed to recently read about the computing power of today’s Tesla: it’s like a data center on wheels! It has more compute power and pulls more power than four of my fully populated racks only 12 years ago.

But the connected car is not standalone. It has to get storage from somewhere. It needs to get secured and be connected to traffic intelligence, GIS, and entertainment data — and that’s going to put pressure on the network providers — including us.

So you can’t have advanced connected cars without edge computing. The edge is key. Yet, contrary to the hype you may have heard, you CANNOT use an edge device for self-driving-car collision-avoidance. To deliver that, you need a split-second response to identify, say, an obstacle in the road, and steer the car away from it. That kind of real-time processing MUST BE performed onboard the car itself.

Edge processing’s key role is reporting car diagnostics: feeding intel back to the data center to figure out if something is wrong with the engine, brakes and other systems. The beauty of edge devices is they can constantly ping the cars and take a load off networks.

And behind all of that will be a data center hub to control all the edge activities. And that hub will have great computing and storage power — and you want that computing centralized so all those apps can work together.

| The cloud vendors love the size, flexibility and carrier connections at large 20 Megawatt+ data centers where they can easily connect. But data centers in ASEAN are much smaller and therefore less desirable for cloud hosting, so how will the giant cloud vendors play in ASEAN? |

The simple answer, Dan, is they will use persistent subsea connectivity back to their primary cloud data center wherever that may be.

Three years ago, I had an opportunity to preview the launch of AWS Outpost, Amazon’s edge platform, and it serves as a model for how other cloud players will connect.

AWS offers service at the edge, but you still need persistent connectivity back to their primary cloud. That’s the only way the product works. At the time, their big pitch was: we’re going to let you run a VMware node. So if you’re a VMware customer, you don’t have to change your architecture. And that VM capability was really exciting for enterprises.

In fact, it’s a game changer. Now the customer who wants to connect to the Amazon cloud simply runs VMware. And if you’re in countries where AWS doesn’t have a cloud, guess what? You need to go subsea to connect.

The advantage that VM gave AWS was you could standardize on a single normal cloud environment, and not have to build forks in your software code. With persistent connectivity, if security gets updated on an AWS cloud, it automatically gets pushed to every Outpost device, so access to the portals, tools and kits are guaranteed.

| Thanks for this great briefing, Jim. You’ve given us a compelling story why managing your multi-vendor cables at Layer 1 enables a lot of flexibility — in serving both data center customers and the big cloud providers. |

Dan, there are a lot of players who will deliver the value in advanced IoT, connected cars, and 5G. Now, we’re not the data center or the chip guy. But if all that stuff has to stay connected and feed back into mega clouds and there’s interaction between clouds and edge nodes, we’re the ones who can provide that.

The software side is not easy. You have to have in-house teams and a certain software-bent to your technical teams and how you think about connecting.

But the reality is: if I have all that intelligence and the ability to control my Layer 1 network and every service that lays on top of that is visible to me, it allows me to optimize the heck out of my network. I also gain the intelligence I need to work out overhead capacity, do capacity planning, and figure out the next regions or cables I want to invest in.

And the more access and control I can give customers, the more services I can get them whether it’s bandwidth, routing protocol at Layer 1, or moving their traffic where they want it to go.

Copyright 2021 Black Swan Telecom Journal

Jim Fagan is Chief Strategy & Revenue Officer at Global Cloud Xchange (GCX). He is a transformative and proven Technology Executive with 20+ years experience spanning across private & public companies, private equity owned to large publicly traded multinational companies across the US, Asia Pacific and China.

Jim has a track record of cross functional success with a strong financial background, deep technical product, operations, sales and general management expertise. He also has an ability to create strategy and operationally deliver while also building and driving disruptive technologies into the market.

He is broadly experienced in Capital Markets — bond and equity — with strong M&A experience including integration.

Considered an industry expert in Cloud, Data Center and Software Defined Networks (SDN), Jim frequently speaks at industry leading events.

Recent Stories

- Epsilon’s Infiny NaaS Platform Brings Global Connection, Agility & Fast Provision for IoT, Clouds & Enterprises in Southeast Asia, China & Beyond — interview with Warren Aw , Epsilon

- PCCW Global: On Leveraging Global IoT Connectivity to Create Mission Critical Use Cases for Enterprises — interview with Craig Price , PCCW Global

- Subex Explains its IoT Security Research Methods: From Malware & Coding Analysis to Distribution & Bad Actor Tracking — interview with Kiran Zachariah , Subex

- Mobile Security Leverage: MNOs to Tool up with Distributed Security Services for Globally-Connected, Mission Critical IoT — interview with Jimmy Jones , Positive Technologies

- TEOCO Brings Bottom Line Savings & Efficiency to Inter-Carrier Billing and Accounting with Machine Learning & Contract Scanning — interview with Jacob Howell , TEOCO

- PRISM Report on IPRN Trends 2020: An Analysis of the Destinations Fraudsters Use in IRSF & Wangiri Attacks — interview with Colin Yates , Yates Consulting

- Telecom Identity Fraud 2020: A 36-Expert Analyst Report on Subscription Fraud, Identity, KYC and Security — by Dan Baker , TRI

- Tackling Telecoms Subscription Fraud in a Digital World — interview with Mel Prescott & Andy Procter , FICO

- How an Energized Antifraud System with SLAs & Revenue Share is Powering Business Growth at Wholesaler iBASIS — interview with Malick Aissi , iBASIS

- Mobileum Tackles Subscription Fraud and ID Spoofing with Machine Learning that is Explainable — interview with Carlos Martins , Mobileum