| © 2022 Black Swan Telecom Journal | • | protecting and growing a robust communications business | • a service of | |

|

|

| Email a colleague |

July 2011

The NetCracker 2010 Global Service Provider Survey: An Independent Analysis

Recently, NetCracker Technology Corp. hired Technology Research Institute (TRI) to deliver an independent analysis and interpretation of its 2010 Global Service Provider Survey.

NetCracker gave TRI total access to the raw data and full rein to normalize and analyze it as we saw fit.

Frankly we didn’t know what to expect because so many surveys these days are put together hastily and circulated to anyone who will answer them. We were pleasantly surprised to find that this one reached a high-level audience. The responses came from CSP organizations, and most of the respondents were executives and industry thought leaders — in fact, many are the same people who make speeches or participate in panels at TM Forum and other, similar events.

The vast majority of respondents came from large- to mid-sized operators. About half were from Tier 1 operators, those with over $10 billion in annual revenue. About a third were from Tier 2 carriers. Only 8 carriers were Tier 3s, with the smallest one in the $200 million annual revenue range.

Given the size of the companies responding, it’s not surprising that “Converged operator“ was the largest category. “Converged” and “Mobile“ operators combined made up roughly 85 percent of the audience. Another 15 percent were “Fixed operators” only.

In terms of geographic regions, the largest segment was from Europe, making up half the audience, followed by North America with about 40 percent. A scattering of surveys also came in from the Middle East, Latin America, and Asia.

The Survey Questions

One of the virtues of NetCracker’s survey was the fact that it didn’t try to accomplish too much. It consisted of three questions only — but these questions definitely nailed the critical issues of the day.

Participants were sent three multiple choice questions that asked them to identify:

- Top 3 Priorities for their CSP business over the next 12 months

- Top 3 Growth Opportunities expected for their business

- Top 3 Competitive Threats to the business

Of these questions, “Priorities“ was the most immediately relevant to people with OSS/BSS responsibilities, so we expect that these responses reflect the greatest accuracy. For the “Growth Opportunities” and “Threats to the Business“ questions, respondents essentially gave us their “interested observer” perspectives on larger business issues outside the OSS/BSS domain.

To better see the contrast of opinions in the survey, we chose to focus on what respondents reported to be their No. 1 Priority, Growth Opportunity or Threat. So let’s see what the survey tells us.

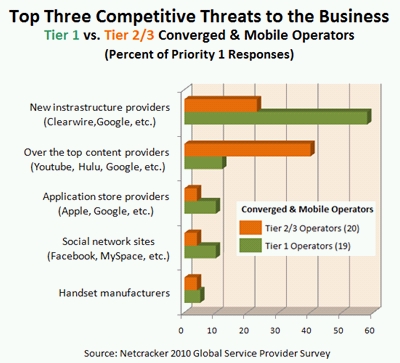

Top Competitive Threats to the Business

The first question asked, “What do you consider to be the top 3 competitive threats to your business?“ This question was especially geared to the problems faced by Converged and Mobile carriers. The chart below shows the answers as they cut across two segments: Tier 1 and Tier 2/3 Converged and Mobile operators.

The results show that Tier 1 and Tier 2/3 carriers have significantly different opinions on what they believe to be the biggest threat. Fifty-five percent of Tier 1 operators felt that “New infrastructure providers“ were the most significant business threat. Tier 2/3 operators felt that “Over the top content providers” were the biggest danger.

Tier 1 carriers are generally the share leaders in their markets. They often acquire smaller operators to gradually expand their footprint and maintain a commanding position on the competitive battlefield. What they are least prepared for are the new infrastructure players who basically use guerilla tactics — launch new business models that disrupt the status quo. Clearwire and Google are certainly companies who are good at that.

Another thing that’s in the back of everyone’s mind in wireless is the hugely disruptive force that Wi-Fi and femtocells may someday bring to the market. Femtocell (or picocell) is a micro-cellular, neighborhood-based technology that could one day divert traffic away from established carriers.

In the same vein, Nokia Siemens announced at the CTIA show in March 2011, a new architecture that it calls Liquid Radio. Liquid Radio directs mobile broadband capacity to where it is needed most. Well, if radio network access becomes more “liquid,“ then it might just flow away from the large incumbents and toward Wi-Fi operators and the like.

So Tier 1 operators are concerned about “new infrastructure“ players for good reason.

The Tier 2/3 operators, meanwhile, are anxious about the threat of “Over the top content providers.“ OTT players are a threat from two directions. First, they compete directly with operators in the sale of content. And just as problematic is the high bandwidth load that OTT players bring to mobile broadband. YouTube videos are free to the user, but are very costly for an operator to deliver. This is why Tier 2/3 operators will be eager to get their hands on advanced network policy enforcement software that will give them better control over where their bandwidth is going.

App stores, social network sites and handset manufacturers are highly visible in the wireless market, but according to survey respondents, they are of less concern as competitors.

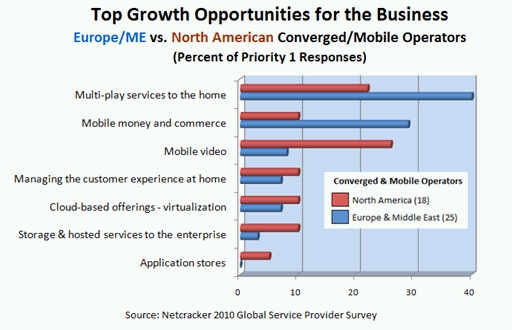

Top Growth Opportunities for the Business

The second question asked, “What are the top 3 growth opportunities that you see in your business?“

Here we found that the most interesting segments to contrast were operators in Europe and the Middle East versus operators in North America.

Living in the United States where the cable industry is very well established and 80 or more TV channels are available even in rural markets, it’s tempting to believe that video doesn’t have much room to grow. Well, the NetCracker survey certainly suggests that this is flawed thinking: Video markets actually seem ready to explode given that almost 40 percent of European/Middle Eastern respondents rated “Multi-play services to the home“ as their No. 1 priority. Cable operators are relatively weak on the continent, so it’s an area where telecom operators are keen to add value.

Another big growth area in Europe and the Middle East is “Mobile money and commerce.“ Almost 30 percent of respondents considered mobile money to be their No. 1 priority. Banking is more mature and cheaper in the U.S. and Canada, and most people have several plastic cards in their wallets. In Europe, however, fees are higher and customer service is not as good, so operators sense an opportunity. Another factor contributing to the excitement over mobile money is the fact that European MVNOs in the retail market are ramping up. The largest grocery retailer in the U.K., Tesco, has more than 2 million customers, and Tesco actively promotes visits to its stores via the handset. If wireless-delivery store coupons become more popular, it’s easy to see why mobile money and commerce will be a big winner.

A rather surprising finding in the survey is that “Mobile video“ is considered the No. 1 growth opportunity by 25 percent of North American respondents. One would have thought that Americans and Canadians had plenty of outlets for watching movies and TV, but apparently, the more the merrier.

One company that’s spiking demand for video is Netflix. Netflix’s original claim to fame was its popular movie rental service sending DVDs via the U.S. postal service. But now Netflix is leveraging proprietary streaming technology to deliver videos via cable and wireless devices. Fortune Magazine named Netflix CEO Reed Hastings as its 2010 Business Person of the Year, beating out Steve Jobs, who came in second place. Netflix’s stock has also been climbing fast since early 2010.

Less than 10 percent of Converged and Mobile operator respondents felt there were as many growth opportunities in “Cloud-based offerings — virtualization“ and “Storage & hosted services to the enterprise.” However, a very respectable 40 percent of Fixed operators considered cloud offerings to be the No. 1 growth opportunity. (Note: That figure is not shown in the chart at the beginning of this section.)

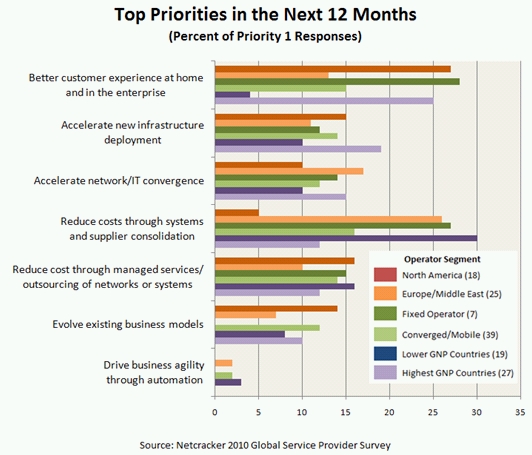

Top Priorities in the Next 12 Months

The third question asked, “What are your top 3 priorities in the next 12 months?“

The answers should be of great interest to folks in the OSS/BSS camp, so we broke out the data into six segments comparing: North America vs. Europe/Middle East; Fixed vs. Converged/Mobile operators; and Higher vs. Lower Gross National Product per Capita in the country where the telecom operates.

The “Priorities“ question raises several interesting points. First, let’s go to the lowest priority: “Drive business agility through automation.” Normally you’d expect that choice to be rated high because it’s the heart of what an OSS/BSS is designed to deliver.

Yet that choice was the lowest overall: Hardly anyone called it a top priority. This response suggests that operators are being very pragmatic in tough times. Today, OSS/BSS investments are focused on solving big business problems — reducing costs or delivering a better customer experience — and not on achieving greater operating efficiency.

While not rated very high in any particular segment, “Evolve existing business models“ is an interesting choice to examine. If your company is struggling to find new directions to turn to in future markets, then you rate this a high priority.

The relatively high number of responses by North American and Converged/Mobile operators in the “business model“ says that business is moving very quickly for those companies.

Turning now to the hot priority areas, we find that there are some striking contrasts in the data. Among the highest ranking priorities is “Reduce costs through systems and supplier consolidations.“ That area is rated very high by European operators (26 percent), Fixed operators (27 percent), and operators in countries on the second tier of GNP per capita (30 percent).

But only 5 percent of North American operators rated consolidation high, which is one-fifth the rating in Europe. For a software vendor, North America is one of the toughest markets in the world to compete in because Canada and the U.S. make up a vast market united by a common language and laws that promote competition. The price that Europeans pay for their OSS/BSS software is generally much higher because it’s hard to standardize across dozens of countries with so many languages and diverse regulations.

Another factor here: Many of the largest North American operators have gone through massive consolidation programs in recent years, so consolidation no longer holds the urgency it once did. In any case, it looks like there’s plenty of pent up demand for consolidation in Europe.

But interestingly, North America leads Europe in the priority placed on “Reducing cost through managed services/outsourcing,“ which suggests that the trend toward SaaS and cloud solutions may be further along in North America.

The priorities given to “Improving the customer experience“ are also wildly different across markets. In the wealthy countries, operators seem eager to spend money on better network quality and customer care since 25 percent rated the customer experience their highest priority. By contrast, only 4 percent of operators in the less wealthy countries made customer experience a top priority, and this difference probably reflects the lower ARPU and profit margins that operators in the less wealthy markets contend with.

The same argument can be made for spending on “Accelerating new infrastructure deployment.“ Eighteen percent of operators in the rich countries think that’s the highest priority, but only 10 percent of operators in the less wealthy countries seem to be putting money there.

On the whole, “Accelerating network/IT convergence“ falls somewhere in the middle. It’s not considered a high priority, and at the same time, it’s not very low. European operators seem highly interested in this area though, which in part may be due to bill-shock regulations that require better integration between BSS and the network. As mobile broadband expands rapidly in Europe, network/IT convergence will also be required to implement network policies and quickly adjust service fees and thereby strike a balance between higher service quality and a desire to not throw money away buying too many routers and switches.

This article first appeared in Billing and OSS World.

Copyright 2011 Black Swan Telecom Journal

Dan Baker is research director of Technology Research Institute (TRI) and editor of the Black Swan Telecom Journal.

Technology Research Institute (TRI) has been writing analyst reports and researching telecom software and systems markets since 1994.

For the last several years, TRI has been following developments in telecom Fraud Management, Revenue Assurance and Analytics solutions.

Most recently, TRI is exploring telecom opportunities in IoT, connectivity, AI/ML and edge computing (4G and 5G) in the Asia Pacific market. Contact Dan via

Black Swan Solution Guides & Papers

- Expanding the Scope of Revenue Assurance Beyond Switch-to-Bill’s Vision — Araxxe — How Araxxe’s end-to-end revenue assurance complements switch-to-bill RA through telescope RA (external and partner data) and microscope RA (high-definition analysis of complex services like bundling and digital services).

- Lanck Telecom FMS: Voice Fraud Management as a Network Service on Demand — Lanck Telecom — A Guide to a new and unique on-demand network service enabling fraud-risky international voice traffic to be monitored (and either alerted or blocked) as that traffic is routed through a wholesaler on its way to its final destinations.

- SHAKEN / STIR Calling Number Verification & Fraud Alerting — iconectiv — SHAKEN/STIR is the telecom industry’s first step toward reviving trust in business telephony — and has recently launched in the U.S. market. This Solution Guide features commentary from technology leaders at iconetiv, a firm heavily involved in the development of SHAKEN.

- Getting Accurate, Up-to-the-Minute Phone Number Porting History & Carrier-of-Record Data to Verify Identity & Mitigate Account Takeovers — iconectiv — Learn about a recently approved risk intelligence service to receive authoritative and real-time notices of numbers being ported and changes to the carrier-of-record for specific telephone numbers.

- The Value of an Authoritative Database of Global Telephone Numbers — iconectiv — Learn about an authoritative database of allocated numbers and special number ranges in every country of the world. The expert explains how this database adds value to any FMS or fraud analyst team.

- The IPRN Database and its Use in IRSF & Wangiri Fraud Control — Yates Fraud Consulting — The IPRN Database is a powerful new tool for helping control IRSF and Wangiri frauds. The pioneer of the category explains the value and use of the IPRN Database in this 14-page Black Swan Solution Guide.

- A Real-Time Cloud Service to Protect the Enterprise PBX from IRSF Fraud — Oculeus — Learn how a new cloud-based solution developed by Oculeus, any enterprise can protect its PBX from IRSF fraud for as little as $5 a month.

- How Regulators can Lead the Fight Against International Bypass Fraud — LATRO Services — As a regulator in a country infected by SIM box fraud, what can you do to improve the situation? A white paper explains the steps you can and should you take — at the national government level — to better protect your country’s tax revenue, quality of communications, and national infrastructure.

- Telecom Identity Fraud 2020: A 36-Expert Analysis Report from TRI — TRI — TRI releases a new research report on telecom identity fraud and security. Black Swan readers can download a free Executive Summary of the Report.

- The 2021 State of Communications-Related Fraud, Identity Theft & Consumer Protection in the USA — iconectiv — This 49-page free Report on communications-related fraud analyzes the FTC’s annual Sentinel consumer fraud statistics and provides a sweeping view of trends and problem areas. It also gives a cross-industry view of the practices and systems that enable fraud control, identity verification, and security in our “zero trust” digital world.

Related Stories

- Dogfight in the Cloud: Time Warner Cable Maneuvers Its Ethernet & Bigger Footprint to Win Enterprise Biz — interview with Jitesh Bhayani — Service provider competition in the U.S. is steadily shifting to the advanced cloud, data center, and connectivity needs of large enterprise. Hear how an MSO has joined the dogfight armed with Ethernet, a national footprint, and SLA guarantees.

- The NetCracker 2010 Global Service Provider Survey: An Independent Analysis — by Dan Baker — Technology Research Institute (TRI) analyzes a Netcracker survey of 50 global B/OSS managers and executives at mid- to large-sized CSPs. The article interprets their view of business challenges, growth opportunities, and competitive threats.

Related Articles

- Wireless Providers Beware: A New Sheriff is Coming to Town... Apple — by Brian Silvestri — Apple’s new iPhone Upgrade Program allows subscribers to buy unlocked phones and once-a-year upgrades direct from Apple stores. A wireless business consultant discusses the threat and the options carriers have to maintain their position in the consumer ecosystem.

- Dogfight in the Cloud: Time Warner Cable Maneuvers Its Ethernet & Bigger Footprint to Win Enterprise Biz — interview with Jitesh Bhayani — Service provider competition in the U.S. is steadily shifting to the advanced cloud, data center, and connectivity needs of large enterprise. Hear how an MSO has joined the dogfight armed with Ethernet, a national footprint, and SLA guarantees.

- Network Pioneer Explains the Tech Shift & Fresh Business Models Driving NFV/SDN — interview with Moshe Shimon — Software Defined Networks (SDN) and Network Function Virtualization (NFV) are revolutionizing the world of telco networks. Now, a Carrier Ethernet equipment provider is among the first to fully support these trends. The interview clears away the confusion and explains the many technical repercussions and business opportunities that are driving SDN/NFV.

- Mobile Business Shock: Device-Driven Research Spots Revenue-Impacting Trends — interview with Chris Hill — OTT players and mobile apps have brought great unpredictability to the network profitability equation. But now, using a mobile crowd sourcing solution serving millions of subscribers, market research intelligence now enables operators to measure the usage uptake of cellular networks vs. WiFi, Facebook vs. Google+, and T-Mobile vs. EPlus.

- Mobile Money: An Expert View of Where It’s Headed and Telecom’s Likely Role — interview with David Birch — Few topics are as muddled or wrapped up with as much hype as telecom’s potential role in mobile money and mobile payments. In this interview, a global expert discusses a broad range of topics: mobile vs. credit cards; fraud concerns; a Kenyan case study; the regulatory climates of Europe and the U.S.; the battle between banks and retailers; and and the considerable value a mobile wallet has even when there’s no money in it.

- Analytics Pioneer: Price Jockeying is an Old Tactic; Fresh Service Ideas Key to Telco Value Creation — interview with David Leshem — Can billing innovation sustain the telecom industry in an age of fierce competition from service providers and Over-the-Top players? An analytics pioneers weighs in on the issue and explains why complex pricing schemes don‘t have a bright future. Using anecdotes and personal stories, he shows why the answer lies in fresh, innovative services, the kind that comes from thinking totally outside the telecom box.

- The NetCracker 2010 Global Service Provider Survey: An Independent Analysis — by Dan Baker — Technology Research Institute (TRI) analyzes a Netcracker survey of 50 global B/OSS managers and executives at mid- to large-sized CSPs. The article interprets their view of business challenges, growth opportunities, and competitive threats.

- Pumping Gold Through Dumb Pipes: Creating Value Streams for Over-The-Top Partners — interview with Steve Cotton — Why worry about business lost to over-the-top (OTT) players when operators can grow the larger pie by focusing on where a CSP adds to the overall “value stream”. This article explains how telecoms can successfully leverage their customer intelligence to deliver narrow-casting, better marketing, timely pricing — often delivering these as a service to the OTT partner.